SUBHEAD: Bitcoin mining industry is now using enough electricity to power 2.26 million American homes.

By Tyler Durden on 5 November 2017 for Zero Hedge -

(http://www.zerohedge.com/news/2017-11-04/each-bitcoin-transaction-uses-much-energy-your-house-week)

Image above: Illustration of Bitcoin's impact on the power grid. From (https://news.bitcoin.com/bitcoin-mining-power-growing-bigger-but-greener/).

[Note from IB Publisher: Each Bitcoin transaction costs as much running the average American home for a week. That is a lot to burn for a Statbuck's coffee and a scone.]

While Bitcoin bulls will probably never have it so good as they have in 2017, we wonder whether many of them have stopped to think about the environmental downside of this roaring bull market.

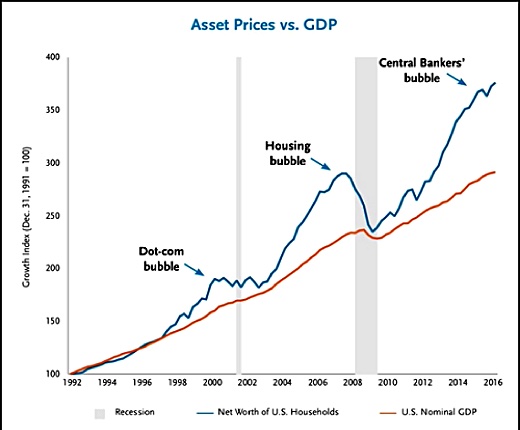

After all, back in the dot.com boom, people had ideas about potential internet businesses, issued pieces of paper representing ownership and watched their prices go parabolic parabolic.

All it took was a Powerpoint presentation, some computer programming expertise and a “research” report, courtesy of Mary Meeker, Henry Blodgett et al.

The environmental downside we’re referring to in Bitcoin is, of course, is energy.

We alluded to this in a constructive way here when we noted that a new Bitcoin mining hub is developing in Iceland, where the natural temperature dramatically reduces the cost of cooling computing hardware.

The primary energy requirement, however, goes into the computing power to “mine” the Bitcoins. The Bitcoin mining industry can consume 24 terawatt hours of electricity and still be profitable – the Motherboard website provides some context...

Bitcoin's incredible price run to break over $7,000 this year has sent its overall electricity consumption soaring, as people worldwide bring more energy-hungry computers online to mine the digital currency.

An index from cryptocurrency analyst Alex de Vries, aka Digiconomist, estimates that with prices the way they are now, it would be profitable for Bitcoin miners to burn through over 24 terawatt-hours of electricity annually as they compete to solve increasingly difficult cryptographic puzzles to "mine" more Bitcoins.

That's about as much as Nigeria, a country of 186 million people, uses in a year… De Vries also estimates that the worldwide Bitcoin mining industry is now using enough electricity to power 2.26 million American homes.

A rapid “Google” later and we discovered that there are 125.8 million American households, so almost 2%.

Another way of looking at Bitcoin’s energy consumption is divide the electricity use in Bitcoin mining each day by the number of daily Bitcoin transactions. As the Motherboard notes, each Bitcoin transaction now requires the same amount of electricity needed to power the average American household for one week.

Expressing Bitcoin's energy use on a per-transaction basis is a useful abstraction. Bitcoin uses x energy in total, and this energy verifies/secures roughly 300k transactions per day. So this measure shows the value we get for all that electricity, since the verified transaction (and our confidence in it) is ultimately the end product…

This averages out to a shocking 215 kilowatt-hours (KWh) of juice used by miners for each Bitcoin transaction (there are currently about 300,000 transactions per day).

Since the average American household consumes 901 KWh per month, each Bitcoin transfer represents enough energy to run a comfortable house, and everything in it, for nearly a week.

Since 2015, Bitcoin's electricity consumption has been very high compared to conventional digital payment methods. This is because the dollar price of Bitcoin is directly proportional to the amount of electricity that can profitably be used to mine it.

Unfortunately for the environmentalists, the Bitcoin price – as every bull knows – entered the parabolic phase in 2017. This Bloomberg chart calculates the number of days for each $1,000 rise in price.

While Motherboard states that De Vries model isn’t perfect and “makes assumptions about the economic incentives available to miners at a given price level”, the website makes the point that there is clearly a “problem”. According to Motherboard...

That problem is carbon emissions. De Vries has come up with some estimates by diving into data made available on a coal-powered Bitcoin mine in Mongolia.

He concluded that this single mine is responsible for 8,000 to 13,000 kg CO2 emissions per Bitcoin it mines, and 24,000 - 40,000 kg of CO2 per hour. As Twitter user Matthias Bartosik noted in some similar estimates, the average European car emits 0.1181 kg of CO2 per kilometer driven.

So for every hour the Mongolian Bitcoin mine operates, it's responsible for (at least) the CO2 equivalent of over 203,000 car kilometers traveled.

However, you’ve probably been thinking what we’ve been thinking. While the price is going parabolic now, Bitcoin usage might go parabolic in the future, problem solved. While it might help, De Vries pointed out the structural flaw...

This gets to the heart of Bitcoin's core innovation, and also its core compromise. In order to achieve a functional, trustworthy decentralized payment system, Bitcoin imposes some very costly inefficiencies on participants, for example voracious electricity consumption and low transaction capacity.

Proposed improvements, like SegWit2x, do promise to increase the number of transactions Bitcoin can handle by at least double, and decrease network congestion.

But since Bitcoin is thousands of times less efficient per transaction than a credit card network, it will need to get thousands of times better.

In the context of climate change, raging wildfires, and record-breaking hurricanes, it's worth asking ourselves hard questions about Bitcoin's environmental footprint, and what we want to use it for.

Do most transactions actually need to bypass trusted third parties like banks and credit card companies, which can operate much more efficiently than Bitcoin's decentralized network?

Imperfect as these financial institutions are, for most of us, the answer is very likely no.

It’s certainly food for thought, even for die-hard libertarians, like ourselves. Then again, perhaps less so for libertarians who’ve been loaded up with Bitcoins in the past few weeks. They would likely be more interested in the bull, bear and neutral cases for Bitcoin in the Bloomberg article linked above. Here is the summary.

With the rhetoric for and against heating up this week amid bitcoin’s barrelling gains, here’s a look at where some big names in finance stand -- from those who see it as the natural evolution of money, to the naysayers waiting for the asset to crash and burn.

Bitcoin’s Backers

.

By Tyler Durden on 5 November 2017 for Zero Hedge -

(http://www.zerohedge.com/news/2017-11-04/each-bitcoin-transaction-uses-much-energy-your-house-week)

Image above: Illustration of Bitcoin's impact on the power grid. From (https://news.bitcoin.com/bitcoin-mining-power-growing-bigger-but-greener/).

[Note from IB Publisher: Each Bitcoin transaction costs as much running the average American home for a week. That is a lot to burn for a Statbuck's coffee and a scone.]

While Bitcoin bulls will probably never have it so good as they have in 2017, we wonder whether many of them have stopped to think about the environmental downside of this roaring bull market.

After all, back in the dot.com boom, people had ideas about potential internet businesses, issued pieces of paper representing ownership and watched their prices go parabolic parabolic.

All it took was a Powerpoint presentation, some computer programming expertise and a “research” report, courtesy of Mary Meeker, Henry Blodgett et al.

The environmental downside we’re referring to in Bitcoin is, of course, is energy.

We alluded to this in a constructive way here when we noted that a new Bitcoin mining hub is developing in Iceland, where the natural temperature dramatically reduces the cost of cooling computing hardware.

The primary energy requirement, however, goes into the computing power to “mine” the Bitcoins. The Bitcoin mining industry can consume 24 terawatt hours of electricity and still be profitable – the Motherboard website provides some context...

Bitcoin's incredible price run to break over $7,000 this year has sent its overall electricity consumption soaring, as people worldwide bring more energy-hungry computers online to mine the digital currency.

An index from cryptocurrency analyst Alex de Vries, aka Digiconomist, estimates that with prices the way they are now, it would be profitable for Bitcoin miners to burn through over 24 terawatt-hours of electricity annually as they compete to solve increasingly difficult cryptographic puzzles to "mine" more Bitcoins.

That's about as much as Nigeria, a country of 186 million people, uses in a year… De Vries also estimates that the worldwide Bitcoin mining industry is now using enough electricity to power 2.26 million American homes.

A rapid “Google” later and we discovered that there are 125.8 million American households, so almost 2%.

Another way of looking at Bitcoin’s energy consumption is divide the electricity use in Bitcoin mining each day by the number of daily Bitcoin transactions. As the Motherboard notes, each Bitcoin transaction now requires the same amount of electricity needed to power the average American household for one week.

Expressing Bitcoin's energy use on a per-transaction basis is a useful abstraction. Bitcoin uses x energy in total, and this energy verifies/secures roughly 300k transactions per day. So this measure shows the value we get for all that electricity, since the verified transaction (and our confidence in it) is ultimately the end product…

This averages out to a shocking 215 kilowatt-hours (KWh) of juice used by miners for each Bitcoin transaction (there are currently about 300,000 transactions per day).

Since the average American household consumes 901 KWh per month, each Bitcoin transfer represents enough energy to run a comfortable house, and everything in it, for nearly a week.

Since 2015, Bitcoin's electricity consumption has been very high compared to conventional digital payment methods. This is because the dollar price of Bitcoin is directly proportional to the amount of electricity that can profitably be used to mine it.

Unfortunately for the environmentalists, the Bitcoin price – as every bull knows – entered the parabolic phase in 2017. This Bloomberg chart calculates the number of days for each $1,000 rise in price.

While Motherboard states that De Vries model isn’t perfect and “makes assumptions about the economic incentives available to miners at a given price level”, the website makes the point that there is clearly a “problem”. According to Motherboard...

That problem is carbon emissions. De Vries has come up with some estimates by diving into data made available on a coal-powered Bitcoin mine in Mongolia.

He concluded that this single mine is responsible for 8,000 to 13,000 kg CO2 emissions per Bitcoin it mines, and 24,000 - 40,000 kg of CO2 per hour. As Twitter user Matthias Bartosik noted in some similar estimates, the average European car emits 0.1181 kg of CO2 per kilometer driven.

So for every hour the Mongolian Bitcoin mine operates, it's responsible for (at least) the CO2 equivalent of over 203,000 car kilometers traveled.

However, you’ve probably been thinking what we’ve been thinking. While the price is going parabolic now, Bitcoin usage might go parabolic in the future, problem solved. While it might help, De Vries pointed out the structural flaw...

As goes the Bitcoin price, so goes its electricity consumption, and therefore its overall carbon emissions. I asked de Vries whether it was possible for Bitcoin to scale its way out of this problem.Motherboard reflects on the cost of Bitcoin’s environmental footprint versus the benefits of a decentralized payment system which avoids the “Too Big To Fails” and their smaller brethren.

"Blockchain is inefficient tech by design, as we create trust by building a system based on distrust. If you only trust yourself and a set of rules (the software), then you have to validate everything that happens against these rules yourself. That is the life of a blockchain node," he said via direct message.

This gets to the heart of Bitcoin's core innovation, and also its core compromise. In order to achieve a functional, trustworthy decentralized payment system, Bitcoin imposes some very costly inefficiencies on participants, for example voracious electricity consumption and low transaction capacity.

Proposed improvements, like SegWit2x, do promise to increase the number of transactions Bitcoin can handle by at least double, and decrease network congestion.

But since Bitcoin is thousands of times less efficient per transaction than a credit card network, it will need to get thousands of times better.

In the context of climate change, raging wildfires, and record-breaking hurricanes, it's worth asking ourselves hard questions about Bitcoin's environmental footprint, and what we want to use it for.

Do most transactions actually need to bypass trusted third parties like banks and credit card companies, which can operate much more efficiently than Bitcoin's decentralized network?

Imperfect as these financial institutions are, for most of us, the answer is very likely no.

It’s certainly food for thought, even for die-hard libertarians, like ourselves. Then again, perhaps less so for libertarians who’ve been loaded up with Bitcoins in the past few weeks. They would likely be more interested in the bull, bear and neutral cases for Bitcoin in the Bloomberg article linked above. Here is the summary.

With the rhetoric for and against heating up this week amid bitcoin’s barrelling gains, here’s a look at where some big names in finance stand -- from those who see it as the natural evolution of money, to the naysayers waiting for the asset to crash and burn.

Bitcoin’s Backers

.